By Stéphan Vincent-Lancrin

Senior Analyst and Deputy Head of Division, OECD Directorate for Education and Skills

Many feel that the coronavirus crisis will accelerate the transition to “digital capitalism”. There is little reason to disagree, although some unpredictable politics might sweep in after the crisis. Education is a difficult market for digital companies, as well as for innovators and entrepreneurs. So the trend may be different.

What do figures say? Well, interestingly, there are no official figures. I am not aware of any OECD government that has official statistical data about its investment in innovation, in digital education technology, in education venture capital – about public and private investments trying to change and improve education through entrepreneurial initiatives.

Thanks to some private actors gathering information about the education technology (EdTech) industry, we are not totally blind. They provide very interesting information about what the digital market currently looks like, and good food for thought for post-COVID crisis scenarios.

How much is being invested in EdTech?

Education is mainly a public sector. It involves a series of private actors, schools and universities, many of them “not for profit”, and an industry mainly focused on publishing (targeting parents and students) and training (targeting corporate markets). The size of the education industry is nowhere near the health-related industry, which produces and invents many of the tools and drugs that we are using during the COVID crisis and that will help us get out of it.

To give you an idea, putting information from various sources together (HolonIQ, World Health Organization, Goldman Sachs, Standard & Poors), one can estimate that the market capitalisation of the health sector (that is, the stock market value of its companies) represents about 50% of its value (USD 5 trillion of the 10 trillion spent on health globally). In education, on the other hand, it is less than 2% (about USD 0.15 trillion of its 6 trillion of global expenditure). In itself, market capitalisation does not matter, it may just mean that education companies tend not to be listed. But one may also wonder whether there are enough private actors and enough capital investment to develop the tools and resources that should help improve education. What we have already learnt during the COVID-19 crisis is that education could have used more digital solutions.

Who is investing the most?

Regardless of the crisis, the geography of investment in the innovative part of the EdTech industry is changing fast. One indicator about innovative companies (start-ups) and what they are up to lies in venture capital, that is, the level of investment in innovative entrepreneurial and high-risk, high-potential solutions.

In education, the global venture capital investment has increased significantly over the past few years, going from USD 1.8 billion to 8.2 billion between 2014 and 2018. Overall, in 2018 the focus of this investment was mainly augmented/virtual reality solutions, then robotics, then artificial intelligence and, finally, blockchain. While augmented and virtual reality solutions are expected to remain the top investment, artificial intelligence solutions may reach the second level in the coming years according to analysts. But things may change quickly following the coronavirus crisis depending on which “new normal” we expect to get.

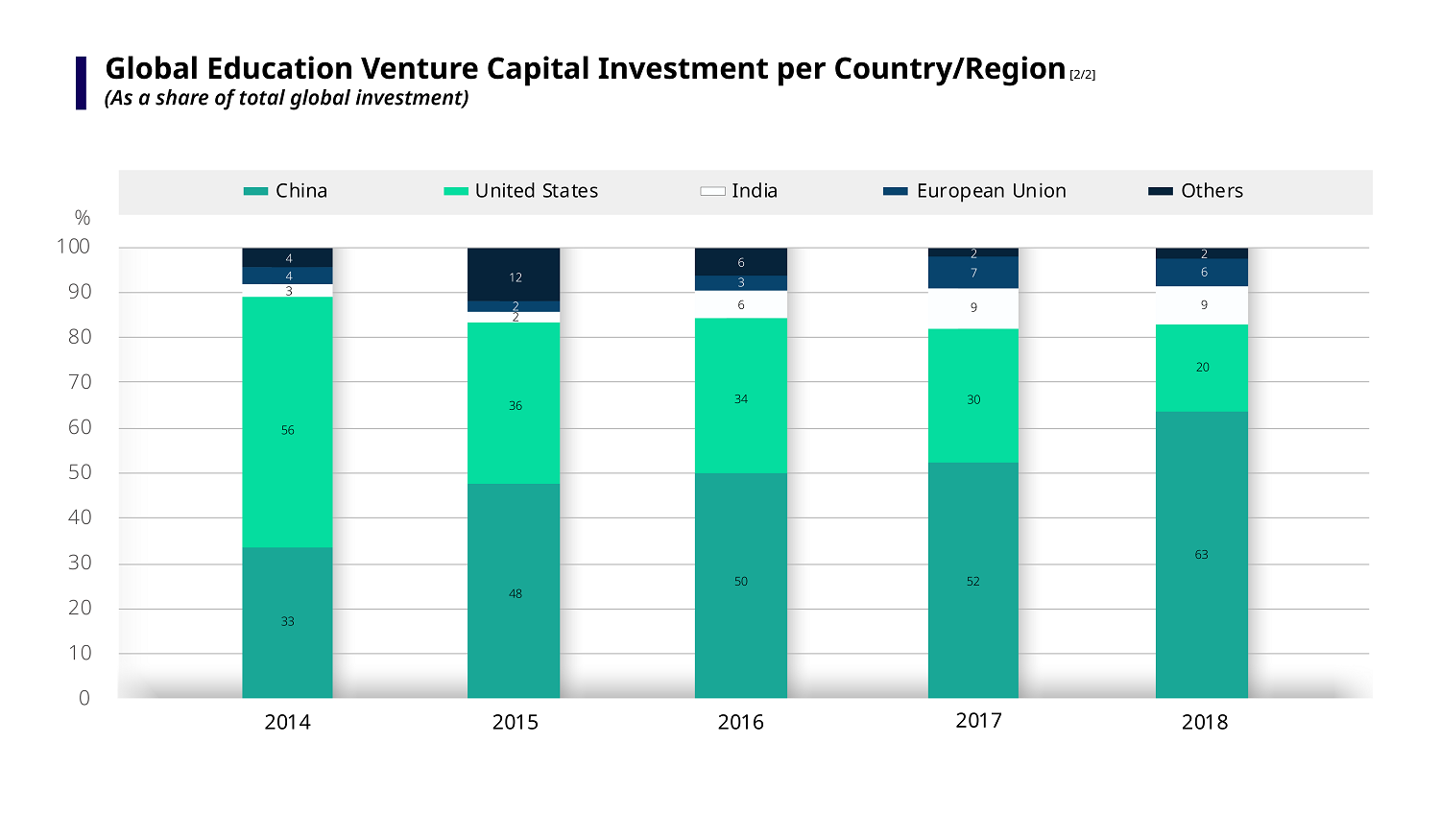

What is striking as well is the geographic shift in the investment. While China invested USD 600 million in 2014, it went up to 5.2 billion in 2018, and over 50% of all global venture capital in education now comes from China. The United States, which used to be the main investor, has increased its investments in past years to reach USD 1.6 billion in 2018 (about 20% of global investment). India has also invested a lot, spending USD 700 million in 2018 on the development of these innovative digital solutions for education, more than the European Union (USD 500 million).

Given that digitalisation has become a general-purpose technology, we could have expected investors across the world to bet that it will disrupt education – and thus to see more similar trends globally.

China and the United States have the largest EdTech footprint. They are also the two countries hosting digital giants. But this does not explain it all, otherwise investment in the United States would have skyrocketed too.

Asia (including China) is peculiar when it comes to education. The world’s two largest education companies globally (by market capitalisation) actually come from China (TAL Education Group [USD 17.7 billion] and New Oriental [USD 11.3 billion]). This creates the business environment for further investment and might explain why the five top unicorns come from India and China (a unicorn is a start-up valued over USD 1 billion). In fact, 7 of the top 10 education unicorns, and 9 out of the 30 largest listed global education companies were Chinese in 2019 – when there were only two in 2013 for the latter.

What’s behind these trends?

There are several possible explanations. The first one is that Chinese (and Asian) families do invest more in education than anywhere else in the world. With an increasing middle class, many education opportunities become more affordable to them. China is the world’s largest digital learning market: it has 172 million online learners (and 142 million mobile learners), with a growth rate above 10% in both categories between 2017 and 2018. A second factor is that the Chinese government as well as local public authorities fully support this trend, notably the “second tier” cities that are eager to get quality education at affordable prices. This represents a massive opportunity for EdTech solutions. A third possible explanation relates to China’s recent history. According to some Chinese friends of mine, rapid economic development over the past 40 years has led to a culture and acceptance of change that makes online solutions not only “tolerable” but even “desirable” to many in China.

In the United States, education is more of a market: the innovative entrepreneurial ecosystems of the country would not let it aside. As a result, the United States is a big player, but it plays with a much smaller and complicated demand.

Why European Union countries invest so little in digital education solutions is a mystery. Perhaps the negotiation of the General Data Protection Regulation (GDPR) and concerns about ethics etc. have been a brake in the past few years? While the United Kingdom was traditionally the top investor, things changed a bit in 2018 with a top five as follows (according to Brighteye Ventures): France (USD 147 million), United Kingdom (142 million), Norway (46 million), Germany (42 million) and Spain (11.4 million).

What role for EdTech post-COVID?

Many of the digital educational solutions based on AI and other learning analytics techniques can only be designed by an EdTech industry. There are some reasons to doubt that there is enough investment in OECD countries, but this is nothing new. As education could have benefited from better and more digital education solutions during the COVID crisis, it may be time to reflect on the role digital technology and an EdTech industry should have in the education sector. Perhaps more than it has currently, perhaps a different one. Some of the solutions that drive the EdTech globally may not be of global interest (test preparation, tutoring and enrichment, English language training and corporate training). But this is how and where the technology is developed, and it offers so much to build on.

Education could have benefited from better and more digital education solutions during the coronavirus crisis – it’s time to reflect on the role digital technology should have in the future of education.

There are (at least) three ways to think about this overall picture. The first is not to bother and just go back to the “same old, same old” after the crisis – to the extent possible… The second is to look at the trends in terms of sovereignty: Will the world want students to be educated online by companies from just a few countries? Tricky discussion. The third is to see the crisis as a new opportunity for international collaboration. A stronger international collaboration in this area – both between companies, but also through international public-private partnerships – might help to provide a better focus and generate common digital goods. This is what we expect to see in the health sector to find quick solutions regarding the coronavirus. Recognised as a public and common good by the international community, education is another area where this could and should be experienced. Let us hope this will be one of the lessons of the crisis.

Read more:

- Coronavirus and the future of learning: What AI could have made possible

- During the coronavirus crisis, children need books more than ever!

- Education disrupted – education rebuilt: Some insights from PISA on the availability and use of digital tools for learning

- How can teachers and school systems respond to the COVID-19 pandemic? Some lessons from TALIS

- The OECD coronavirus (COVID-19) policy hub